Most important CBSE repeated questions in Exams of class 11 microeconomics

Q1. Explain the central problem " what to Produce"?

Ans: What to produce : It is the problem of choosing which commodity to be produced and in what quantity.

the problem of what to produce has two part:

(1) what possible commodity to produce: an economy has to decide, which consumer goods and which of the capital goods are to be produced. in the same way, economy has to make a choice between civil goods and war goods.

(2) How much to produce: After deciding the goods to be produced, economy has to decide the quantity of each commodity, that is selected. It means, it involves a decision regarding the quantity to be produced, of consumer and capital goods, civil and war goods and so on.

Q2. Explain the central problem " for whom to produce"?

Ans: For whom to produce: In this the problem is of choosing the factor pricing. It means that how much of factors of production should be paid in the form of reward for their work in the form of rent, wages, interest and profits.

The problem can be categories into two parts:

(1) personal distribution: It means how national income of an economy is distributed among different groups of people.

(2) Functional distribution: It involves deciding the share of different factor of production in the total national product of the country.

Q3. There is an inverse relationship between price and quantity demanded of a commodity. Explain.

ANS: Here you have to explain Law of demand (Meaning, assumptions, and few examples)

Q4. What is "change in supply"? Explain the effect of tax imposed on a good on the supply of the good?

Ans: Change in supply: It is due to the change in other than price factor like technology, taxation policy etc.

Taxation Policy: If the taxes imposed on production( excises duty) or on sales(sales tax) increases then the profit margin of the producer reduces. Thereby reducing the supply and vice-versa.

Q5. why is the numbers of firms small in an oligopoly market?

Ans: Oligopoly market: It is a market form in which there are few dominant firms interdependent on each other for their decisions. Few firms: Oligopolist are generally few large firms producing the major output. they would have tough competition which would lead to interdependence in terms of price and output.

Q6. Explain" Freedom of entry and exit to the firm in industry" feature of monopolistic competition.

Ans: Monopolistic competition: It is the market structure in which the firms are large in number selling differentiated product.

Free entry and exit of a firm: In this market form, the firms have the freedom to enter or exit anytime from the market.

Because there is free entry and exit of firms, then firms are not able to earn super normal profits in long run nor there is chances of losses. This happen because in the shot run firms earns abnormal profits then due to free entry new firms enter into the market and abnormal profits neutralized to normal profits.

Where as if the firms incurred losses then few firm might exit and market comes back to normal profits.

So we can conclude that in the long run under perfect competition a firm can only earn normal profits.

Q7. What will be the effect on total product and marginal product when one factor is variable and others are constant? Explain with table and diagram.

Ans: In this you have to explain Law of variable Proportion approach

Ans: What to produce : It is the problem of choosing which commodity to be produced and in what quantity.

the problem of what to produce has two part:

(1) what possible commodity to produce: an economy has to decide, which consumer goods and which of the capital goods are to be produced. in the same way, economy has to make a choice between civil goods and war goods.

(2) How much to produce: After deciding the goods to be produced, economy has to decide the quantity of each commodity, that is selected. It means, it involves a decision regarding the quantity to be produced, of consumer and capital goods, civil and war goods and so on.

Q2. Explain the central problem " for whom to produce"?

Ans: For whom to produce: In this the problem is of choosing the factor pricing. It means that how much of factors of production should be paid in the form of reward for their work in the form of rent, wages, interest and profits.

(1) what possible commodity to produce: an economy has to decide, which consumer goods and which of the capital goods are to be produced. in the same way, economy has to make a choice between civil goods and war goods.

(2) How much to produce: After deciding the goods to be produced, economy has to decide the quantity of each commodity, that is selected. It means, it involves a decision regarding the quantity to be produced, of consumer and capital goods, civil and war goods and so on.

Q2. Explain the central problem " for whom to produce"?

Ans: For whom to produce: In this the problem is of choosing the factor pricing. It means that how much of factors of production should be paid in the form of reward for their work in the form of rent, wages, interest and profits.

The problem can be categories into two parts:

(1) personal distribution: It means how national income of an economy is distributed among different groups of people.

(2) Functional distribution: It involves deciding the share of different factor of production in the total national product of the country.

Q3. There is an inverse relationship between price and quantity demanded of a commodity. Explain.

ANS: Here you have to explain Law of demand (Meaning, assumptions, and few examples)

Q4. What is "change in supply"? Explain the effect of tax imposed on a good on the supply of the good?

Ans: Change in supply: It is due to the change in other than price factor like technology, taxation policy etc.

Taxation Policy: If the taxes imposed on production( excises duty) or on sales(sales tax) increases then the profit margin of the producer reduces. Thereby reducing the supply and vice-versa.

Q5. why is the numbers of firms small in an oligopoly market?

Ans: Oligopoly market: It is a market form in which there are few dominant firms interdependent on each other for their decisions. Few firms: Oligopolist are generally few large firms producing the major output. they would have tough competition which would lead to interdependence in terms of price and output.

Q6. Explain" Freedom of entry and exit to the firm in industry" feature of monopolistic competition.

Ans: Monopolistic competition: It is the market structure in which the firms are large in number selling differentiated product.

Free entry and exit of a firm: In this market form, the firms have the freedom to enter or exit anytime from the market.

Because there is free entry and exit of firms, then firms are not able to earn super normal profits in long run nor there is chances of losses. This happen because in the shot run firms earns abnormal profits then due to free entry new firms enter into the market and abnormal profits neutralized to normal profits.

Where as if the firms incurred losses then few firm might exit and market comes back to normal profits.

So we can conclude that in the long run under perfect competition a firm can only earn normal profits.

(1) personal distribution: It means how national income of an economy is distributed among different groups of people.

(2) Functional distribution: It involves deciding the share of different factor of production in the total national product of the country.

Q3. There is an inverse relationship between price and quantity demanded of a commodity. Explain.

ANS: Here you have to explain Law of demand (Meaning, assumptions, and few examples)

Q4. What is "change in supply"? Explain the effect of tax imposed on a good on the supply of the good?

Ans: Change in supply: It is due to the change in other than price factor like technology, taxation policy etc.

Taxation Policy: If the taxes imposed on production( excises duty) or on sales(sales tax) increases then the profit margin of the producer reduces. Thereby reducing the supply and vice-versa.

Q5. why is the numbers of firms small in an oligopoly market?

Ans: Oligopoly market: It is a market form in which there are few dominant firms interdependent on each other for their decisions. Few firms: Oligopolist are generally few large firms producing the major output. they would have tough competition which would lead to interdependence in terms of price and output.

Q6. Explain" Freedom of entry and exit to the firm in industry" feature of monopolistic competition.

Ans: Monopolistic competition: It is the market structure in which the firms are large in number selling differentiated product.

Free entry and exit of a firm: In this market form, the firms have the freedom to enter or exit anytime from the market.

Because there is free entry and exit of firms, then firms are not able to earn super normal profits in long run nor there is chances of losses. This happen because in the shot run firms earns abnormal profits then due to free entry new firms enter into the market and abnormal profits neutralized to normal profits.

Where as if the firms incurred losses then few firm might exit and market comes back to normal profits.

So we can conclude that in the long run under perfect competition a firm can only earn normal profits.

Q7. What will be the effect on total product and marginal product when one factor is variable and others are constant? Explain with table and diagram.

Ans: In this you have to explain Law of variable Proportion approach

Ans: In this you have to explain Law of variable Proportion approach

- Statement: This law stats that as we employ more variable factors over the fixed factors then TP:

(a). First Increase at an increasing rate.

(b). Then increases at a diminishing rate.

(c). And finally starts falling.

- Assumption:

(1). This law applies in short run period only.

(2). All the factors of Production are equally efficient.

(3). Technology remains same.

- Schedule:

- Diagram:

(a). First Increase at an increasing rate.

(b). Then increases at a diminishing rate.

(c). And finally starts falling.

(1). This law applies in short run period only.

(2). All the factors of Production are equally efficient.

(3). Technology remains same.

Stages And Causes:

(a). Increasing Returns To Factors:

1. In this stage TP increases at increasing rate and MP also increases.

2. When production begins and we employ the variable factors over fixed factors it leads to optimum utilization of resources as there division of labour and specialization.

3. I n this stage the fixed factor is utilized to its fullest level.

4. Here variable factor are either less or equal fixed factors capacity.

(b).Diminishing Returns to Factor:

1. In this stage, TP increases at a diminishing rate and MP falls.

2.Here variable factor is more than fixed factor capacity.

3. In this stage, there is use of fixed factor beyond its capacity because of which MP falls.

4.This stage is the "Real Stages of Production" as all the producers like producing in the stage as TP is maximum.

(c).Stage of negative returns to Factors:

1.Here the TP starts falling and MP becomes negative.

2. None of the producer like to produce in this stages, so they stop production as MP is Negative.

3.This happens due to over burdening of fixed factors.

Q8. Explain the condition of consumer's equilibrium with the help of an indifference curve analysis.

Ans: Indifference Curve Approach

- consumer attains equilibrium at the point where budget line is tangent to indifference curve.

MRSxy = Px

Py

OR

MRSxy = MRE

slope of indifference cure = slope of budget line

In the above diagram PT represent budget line and IC1, IC2, IC3 represent different set of satisfactions where IC3 > IC2. Here IC3 is the highest satisfaction but not within the budget of the consumer.Where as IC1 and IC2 are within the budget IC2 > IC1. also budget lines makes a tangent.

In the above diagram PT represent budget line and IC1, IC2, IC3 represent different set of satisfactions where IC3 > IC2. Here IC3 is the highest satisfaction but not within the budget of the consumer.Where as IC1 and IC2 are within the budget IC2 > IC1. also budget lines makes a tangent.

consumer attains equilibrium at the point where budget line is tangent to the indifference curve and IC should be convex to the origin i.e MRS should be diminishing at a point of equilibrium.

MRSxy = Px

Py

OR

MRSxy = MRE

slope of indifference cure = slope of budget line

consumer attains equilibrium at the point where budget line is tangent to the indifference curve and IC should be convex to the origin i.e MRS should be diminishing at a point of equilibrium.

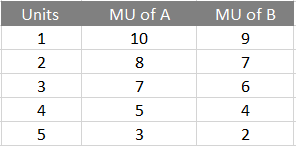

Q9. A consumer consumes two goods X and Y. Explain what will happen if MUx/Px is greater than MUy/Py?

Ans: This situation implies that by spending a rupee more on good x the consumer get x greater MU then in case of good Y. accordingly, he will spend more on 'X' than Y. As consumption of X increases, MUx will fall. on the other hand as consumption of Y falls, MUy wull rise. the consumer will stop buying more of X in place of Y only when MUx/Px = MUy/Py

Q10. Market for a good is in equilibrium. there is simultaneous " increase" in both demand and supply of the good. Explain the effect on market price.

Ans:Increase in demand = increase in supply

Chain effect:When increase in demand is proportionately equal to increase in supply, then rightward shift in demand curve from D to D1 is proportionately equal to rightward shift in supply curve from s to S1. the new equilibrium is determined at E1. As demand and supply increases in the same proportion, equilibrium price remains same at OP,but equilibrium quantity rises from OQ to OQ1.

Q11. Give the Meaning and characteristics of production possibility frontier.

Ans: Meaning: It is a curve which shows all the possible combination of two goods which an economy can produce with given resources and technology. Characteristics:(1) It is downward slopping from left to right because to gain one good we need to sacrifice other good.

(2) It is always concave to the origin due to increasing MOC.

Diagram:

Q9. A consumer consumes two goods X and Y. Explain what will happen if MUx/Px is greater than MUy/Py?

Ans: This situation implies that by spending a rupee more on good x the consumer get x greater MU then in case of good Y. accordingly, he will spend more on 'X' than Y. As consumption of X increases, MUx will fall. on the other hand as consumption of Y falls, MUy wull rise. the consumer will stop buying more of X in place of Y only when MUx/Px = MUy/Py

Q10. Market for a good is in equilibrium. there is simultaneous " increase" in both demand and supply of the good. Explain the effect on market price.

Ans:Increase in demand = increase in supply

Ans: This situation implies that by spending a rupee more on good x the consumer get x greater MU then in case of good Y. accordingly, he will spend more on 'X' than Y. As consumption of X increases, MUx will fall. on the other hand as consumption of Y falls, MUy wull rise. the consumer will stop buying more of X in place of Y only when MUx/Px = MUy/Py

Q10. Market for a good is in equilibrium. there is simultaneous " increase" in both demand and supply of the good. Explain the effect on market price.

Ans:Increase in demand = increase in supply

Chain effect:When increase in demand is proportionately equal to increase in supply, then rightward shift in demand curve from D to D1 is proportionately equal to rightward shift in supply curve from s to S1. the new equilibrium is determined at E1. As demand and supply increases in the same proportion, equilibrium price remains same at OP,but equilibrium quantity rises from OQ to OQ1.

Q11. Give the Meaning and characteristics of production possibility frontier.

Ans: Meaning: It is a curve which shows all the possible combination of two goods which an economy can produce with given resources and technology. Characteristics:(1) It is downward slopping from left to right because to gain one good we need to sacrifice other good.

(2) It is always concave to the origin due to increasing MOC.

Diagram:

Q12. Distinguish between increase n demand and increase in quantity demand of a good.

Ans:

Q13. Explain perfect knowledge about the markets feature of perfect competition.

Ans: Perfect Knowledge: Firms have all the knowledge about product and the market and the buyers are also well informed.

Because there is perfect knowledge at the buyers and sellers end the buyer would not pay more than the uniform price, similarly the seller would not be able to earn more than the price set by industry. uniform prices would prevail.

Q14. Define market supply. Explain the factor input prices that can cause a change in supply.

Ans: Market supply: It refers to the quantity of a commodity which all the sellers in a market are willing to supply at a given price in a given period of time. Change in price of input: If price of inputs or factors of production increases it causes an increases in the cost of production and fall in profit.Therefor the supply falls and vice-versa.

Q15. Explain the meaning of excess demand and excess supply with the help of a schedule. Explain their effect on equilibrium price.

Ans: Case-1 : When there is Excess demand

This means market price is lower than the equilibrium price.

In such a situation the prices would be pushed upward due to which suppliers would like supply more(expansion o Q.S) where as buyers would demand less at higher prices(contraction of Q.D), this would set the equilibrium price.

Case-2 : When there is excess supply

This means market price is higher than equilibrium price.

In such a situation when prices are higher than equilibrium price, the supply would fall, pilling up of stock and now to clear off the stock he would reduces the prices, this would lead to expansion of Q,D and contraction of Q.S and ultimately equilibrium would be attained.

Q16. Explain the conditions of producer's equilibrium under perfect competition.

Ans: MR and MC approach

A Producer attains equilibrium when marginal revenue is equal to the marginal cost and at very next level of output MC is rising.

MR = MC & next output MC should be rising.

MR: It refers to additional revenue generated by selling on additional unit of an output.

MC: It refers to the additional cost incurred on producing an additional unit of an output.

Schedule:

Diagram:

In the diagram MR curve is parallel to x-axis because in perfect competition MR is constant, MC curve is U shaped. MR = MC at point Z and E. but after Z MC is falling whereas after point E MC is rising. therefore at point E producer is said to be at equilibrium because after this level of output if he produce then he would incurred losses.

Q12. Distinguish between increase n demand and increase in quantity demand of a good.

Ans:

Q13. Explain perfect knowledge about the markets feature of perfect competition.

Ans: Perfect Knowledge: Firms have all the knowledge about product and the market and the buyers are also well informed.

Because there is perfect knowledge at the buyers and sellers end the buyer would not pay more than the uniform price, similarly the seller would not be able to earn more than the price set by industry. uniform prices would prevail.

Q14. Define market supply. Explain the factor input prices that can cause a change in supply.

Ans: Market supply: It refers to the quantity of a commodity which all the sellers in a market are willing to supply at a given price in a given period of time. Change in price of input: If price of inputs or factors of production increases it causes an increases in the cost of production and fall in profit.Therefor the supply falls and vice-versa.

Q15. Explain the meaning of excess demand and excess supply with the help of a schedule. Explain their effect on equilibrium price.

Ans: Case-1 : When there is Excess demand

Ans: Market supply: It refers to the quantity of a commodity which all the sellers in a market are willing to supply at a given price in a given period of time. Change in price of input: If price of inputs or factors of production increases it causes an increases in the cost of production and fall in profit.Therefor the supply falls and vice-versa.

Q15. Explain the meaning of excess demand and excess supply with the help of a schedule. Explain their effect on equilibrium price.

Ans: Case-1 : When there is Excess demand

This means market price is lower than the equilibrium price.

In such a situation the prices would be pushed upward due to which suppliers would like supply more(expansion o Q.S) where as buyers would demand less at higher prices(contraction of Q.D), this would set the equilibrium price.

Case-2 : When there is excess supply

This means market price is higher than equilibrium price.

In such a situation when prices are higher than equilibrium price, the supply would fall, pilling up of stock and now to clear off the stock he would reduces the prices, this would lead to expansion of Q,D and contraction of Q.S and ultimately equilibrium would be attained.

Q16. Explain the conditions of producer's equilibrium under perfect competition.

Ans: MR and MC approach

A Producer attains equilibrium when marginal revenue is equal to the marginal cost and at very next level of output MC is rising.

Q17. A consumer consumes only two goods X and Y. explain the conditions of consumer's equilibrium using utility Analysis.

Ans: Double commodity case:

Ans: Double commodity case:

- In this case the consumer consumes two commodities. the condition for equilibrium is:

MUx = MUy = MUm

Px Py

OR

MUx = Px = MUm

MUy Py - In this case price of both the goods are same.

MUx = MUy = MUm

Px Py

Now if Px and Py are equal this means

Px = 1

Py

Assuming, MUm = 1. now the consumer would be at equilibrium when within his income his

MUx =1

MUy

MUy

Assumption is that the consumer has only rupees 5. here if the consumer spends all his rupees 5 on A then he gets 33 utils whereas if he consume all B he gets 28 utils, but in this manner he would be consuming one good.

But if he rupee 1 on A and rupee 2 on B and so on then by spending the 4th and 5th rupee his MU is same from A and B.

MUx = PX = MUm

MUy Py

7 = 1 = 1

7 1 by consuming in such a manner he gets maximum utils.

But if he rupee 1 on A and rupee 2 on B and so on then by spending the 4th and 5th rupee his MU is same from A and B.

MUx = PX = MUm

MUy Py

7 = 1 = 1

7 1 by consuming in such a manner he gets maximum utils.

Q18. what is indifference curve? state three proportties of indifference curves.

Ans: Meaning: It is a curve shows all the possible combination of two goods that gives some level of satisfaction to the consumer.

Ans: Meaning: It is a curve shows all the possible combination of two goods that gives some level of satisfaction to the consumer.

Properties of Indifference Cure :

(1). Indifference cures ae always convex to the origin: An indifference curve to the origin because of diminishing MRS. MRS declines continuously because of the law of diminishing marginal utility. it must be noted that MRS indicates the slope of indifference curve.

(2). Indifference curve slope downwards: It implies that as a consumer more of one goods, he must consume less of the other goods. it happens because if the consumer decides to have more units of one good, he will have to reduce the number of units of another goods, so that utility remains same.

(3). Higher IC represents higher levels of satisfaction : Higher IC represents large bundles of goods which means more utility because of monotonic preferences.Q19. what is meant by price ceiling? Explain its implications.

Ans: Price ceiling : When the government set the price below the equilibrium price to safe guard the interest of consumers.

implications of price ceiling:

(1). Black Market:A black market is any market in which the commodities are sold at a price higher than the maximum price fixed by govt. Black markets exists because consumers are ready to pay a price more than the price fixed by the govt. to get more of limited amount of commodity available.

(2). Difficulty in obtaining goods from ration shops:

Consumers has to stand in long queues to buy goods from ration shops. sometimes, commodity is not able in the ration shops or goods are of inferior quantity.

Q20. Explain the central problem of how to produce with example.

Ans: How to produce: In this the problems of choosing the technique of production i.e to produce by using labour intensive technique or capital intensive technique.

The selection technique is made with a view to achieve the objective of raising the standard of living of people and to provide employment to everyone.

Example: In India LIT is preferred due to abundance of labour, where as countries like USA prefer CIT due to shortage of labour and abundance of capital.

Q21. Differentiate between change in supply and change in quantity supplied.

Ans:

Comments

Post a Comment